Questa volta ho messo insieme qualche numero semestrale e delle vendite a fine settembre delle principali case di Champagne, di cui gia’ analizziamo i bilanci, oltre a dare una sbirciatina alle esportazioni di Champagne. Quello che se ne ricava e’ un quadro in deterioramento per tutti quanti. Se nel primo semestre i segnali riguardavano soltanto una azienda (Laurent Perrier, che ha deciso una ristrutturazione della struttura commerciale), nel terzo trimestre, che e’ un periodo “in crescita” per preparare le vendite del quarto trimestre, sia LVMH che Vranken Pommery hanno fatto vedere un calo del 5% delle vendite, entrambe in forte deterioramento rispetto all’andamento del primo semestre (tutto sommato buono, soprattutto dal punto di vista dei margini). E le esportazioni intanto ripiegano: nell’anno mobile a settembre 2008 siamo sotto dell’1%, che significa 1.5% annualizzato. Colpa di chi? Del crollo del 30% delle esportazioni di Champagne nel mercato americano… peccato che il cambio si sia svalutato soltanto del 12-13%…

For today I put together some numbers of H1 and Q3 sales of the major Champagne houses. In addition I gave a look to exports of Champagne. What you get is a picture of gradual deterioration. If in the first half the signals were only visible for one company (Laurent Perrier, which decided a restructuring of the commercial structure) in Q3 (which starts to be an important quarter), LVMH and Vranken Pommery showed a decline of 5% of sales, both with a sharp deterioration compared to the first half (when they performed very well, especially in terms of margins). Meanwhile exports of Champagne are starting to deteriorate: rolling year to September 2008 is down 1% vs. 2007 year end. Where is the problem? The collapse of 30% of exports of Champagne in the American market is clearly the key reason, only partially explained by the 12-13% USD devaluation

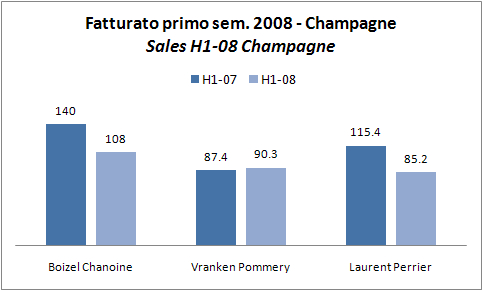

Venendo ai numeri, vi presento i dati di fatturato delle 4 aziende che guardiamo. LVMH, che non e’ nel grafico perche’ troppo grande, ha chiuso il primo semestre a +0.5% (ricordo che c’e’ dentro sia Champagne che vino), da EUR653m a EUR656m. Invece, passando agli operatori speciliazzati, il panorama e’ piu’ vario: Boizel Chanoine mostra un calo sostanziale (-23%), dovuto alla decisione di ridurre le scorte e l’indebitamento: in realta’ le vendite di Champagne sarebbero cresciute del 5% da EUR103m a EUR108m (e come vedremo gli utili operativi si muovono in questa direzione); anzi, Boizel specifica che escludendo anche l’attivita’ della sua controllata che fa trading, le vendite sarebbero cresciute dell’8% e addiritittura dell’11% prima della svalutazione della sterlina. Vranken Pommery invece fa +3.4% (+4.7% per lo Champagne).

Turning to the numbers, we present the sales of 4 companies. LVMH, which is not in the chart because it is too big, closed the first half with +0.5% (please remember that there is Champagne plus wine), from EUR653m to EUR656m. Moving to Champagne houses, the landscape is more varied: Boizel Chanoine shows a substantial decrease (-23%), due to the decision to reduce stocks and debt: in reality Champagne sales (depletions) would grow by 5% From EUR103m to EUR108m (and as we will see operating profits are moving in that direction); indeed, Boizel specifies that excluding the activities of its subsidiary that makes trading, sales would be up by 8% and even 11 % Before the devaluation of the pound. Vranken Pommery did +3.4% (+4.7% for the Champagne).

Invece, Laurent Perrier ha fatto il classico profit warning, stante il riposizionamento commerciale deciso e a causa della congiuntura difficile del mercato. Fatturato in crollo verticale (-26%, -23% prima dei cambi), dovuto a un calo del 40% dei volumi non compensato da un +17% nel prezzo medio di vendita.

Instead, Laurent Perrier has made a profit warning, given the commercial repositioning and the impact of the difficult economic environment. Turnover is in vertical drop (-26%, -23% before foreign exchange), due to a decline of 40% of the volumes not offset by a 17% in average selling price.

Abbiamo soltanto qualche indicazione sull’andamento dei margini di profitto nel primo semestre, quelli di Boizel e di Vranken. In entrambi i casi, gli utili stanno crescendo in modo significativo, anche se i soldi in questo business si fanno tra settembre e dicembre. Il margine operativo di entrambi sale dal 7-8% dello scorso anno (primo semestre) al 12-13% di quest’anno. We have only some indication on profit margins in H1, for Boizel and VRANKEN. In both cases, profits are growing significantly, even if the money in this business are made between September and December. The operating margin for both went from 7-8% last year (first half) to 12-13% this year.

Cosa succede nel terzo trimestre del 2008? Abbiamo l’evidenza di due operatori: LVMH e Vranken Pommery. Purtroppo un’evidenza omogenea, dato che in entrambi i casi si passa da un fatturato leggermente in crescita a una riduzione del 5%, per Vranken Pommery da EUR55m a EUR52m e per LVMH da EUR416m a EUR394m. What happened in Q3-08? We have evidence of two players: LVMH VRANKEN Pommery. Unfortunately evidence is homogeneous, since in both cases it changed from a slight growth in turnover to a reduction of 5%, with Vranken Pommery from EUR55m to EUR52m and LVMH from EUR416m to EUR394m.

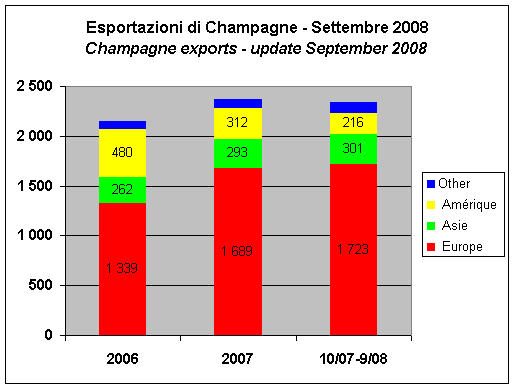

Infine, ho dato un’occhiata alle esportazioni di Champagne come riportate dalla dogana francese. I numeri a fine settembre (12 mesi) confrontati con il 2007 totale mostrano un calo dell’1% da EUR2370m a EUR2342m. Il mercato chiave sta tenendo (Europa +2% a EUR1723m) ma sta cedendo di schianto il mercato americano: da EUR312m si e’ passati nel giro di 9 mesi su un livello di EUR216 (sempre su base annua), cioe’ -31%. Finally, I looked at exports of Champagne as reported by French customs. The numbers at the end of September (12 months) compared with 2007 show a decline of 1% from EUR2370m a EUR2342m. The key market is holding up (Europe +2% to EUR1723m) but the American market is crashing: from EUR312m in 2007 it moved to EUR216 (always on an annual basis), -31% .