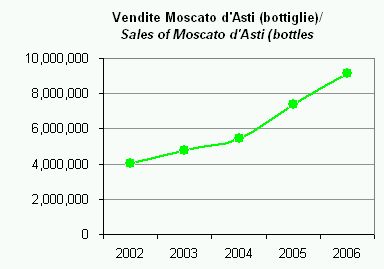

Il commento dei numeri della Ferdinando Giordano Spa è per me fonte di sentimenti contastanti. Da un lato, come sommelier appassionato, non sono un cliente di questa societa’ e tendo a considerare il loro canale distributivo (la vendita diretta) un po’ invasivo. Dall’altro, guardando i numeri non posso che togliermi il cappello e complimentarmi per una azienda che appare ben gestita e, visti i movimenti tra gli azionisti, e’ piuttosto facile che possa essere quotata in Borsa di qui a un paio di anni. Il 2006 e’ stato un altro anno fantastico per Giordano. Il fatturato e’ cresciuto del 18%, con una ulteriore accelerazione rispetto al 2005 (+13%) e sia in Italia (+12% dopo un +19% del 2005) che all’estero (+27%) la societa’ e’ cresciuta in modo molto significativo. Cosi’ il fatturato e’ arrivato a EUR135m, superando Antinori e avvicinandosi a Campari, che dovrebbe essere a circa EUR150m (con l’aiuto significativo del vermouth Cinzano). Anche se inferiore ad altri operatori, Giordano realizza ormai il 40% del fatturato al di fuori dell’Italia (principalmente in Germania, UK e in una fase iniziale di sviluppo sulla East Coast americana).

The comment of 2006 figures of Ferdinando Giordano is not easy for me. As a sommelier and wine enthusiast, I am not a customer of this company and I consider their distribution channel (direct channel) a disturbing one. On the other hand, looking at financial performance I cannot be avoid to be delighted. This is a well managed company, growing strongly and we might soon have it listed on the stock exchange. In 2006 sales grew by 18%, with an acceleration vs. the +13% in 2005, driven by both Italy (12% growth after a + 19%) and a jump in foreign sales (+27%). Even if lower than other operators, Giordano now achieves 40% of its turnover outside Italy (Germany and UK mainly, with a growing weight of US). Giordano revenues are now EUR135m, above Antinori and not far from Campari (EUR150m this year, helped by vermouth).