[English translation at the end of the document]

Fonte: Viniflhor

Viniflhor ha pubblicato un sondaggio molto interessante sulla vendita diretta dei produttori francesi di vino, che ci serve per dare una dimensione a diversi tipi di distribuzione quali internet, la vendita per corrispondenza e, in generale, la vendita diretta. Premettendo che questo sondaggio ha visto una partecipazione di circa il 13% dei questionari inviati (considerato quindi un campione significativo), il quadro e’ il seguente: (1) la vendita diretta rappresenta circa il 16% del fatturato delle aziende ed e’ fatta praticamente da tutte le aziende presso la proprieta’; (2) la vendita diretta rappresenta una quota significativa delle vendite soltanto per le aziende fino a 5000hl di produzione; (3) la vendita via internet e’ messa in pratica solo dal 4% delle aziende (paradossalmente le piu’ grandi e le piu’ piccole, con un ulteriore 17% che dichiara di usare internet come strumento di promozione), ma rappresenta soltanto l’1.4% della vendita diretta, cioe’ una porzione infinitesima di delle vendite. Ancora molta strada da fare.

Per la serie “chi cerca trova”, mi sono messo a guardare in giro se ci sono altre aziende vinicole quotate in borsa (in modo da avere i bilanci senza doverli chiedere). E ho trovato diverse sorprese, almeno per me. La prima che vi espongo oggi e’ quella di una azienda di nome Cottin Freres, di proprieta’ della stessa famiglia, quotata in borsa in Francia con un valore di mercato di EUR18m e attiva in Borgogna. Le dimensioni di questa azienda sono molto piccole, dato che fattura meno di EUR50m all’anno. Proprio per questo e’ interessante seguirla e, gia’ vi anticipo, ce ne sono altre. I have just found a number of interesting small listed wine companies around, with a few surprises. The first one I am introducing today is Cottin Freres, which is a family owned business in Burgundy with a market capitalization of EUR18m. The size of this company with less than 50m sales is very interesting because it can be directly compared with Italian ones.7

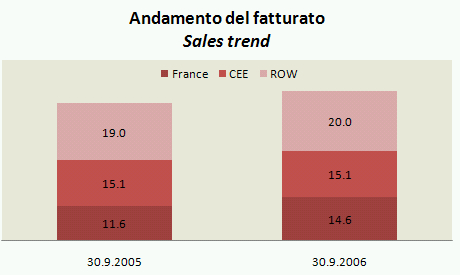

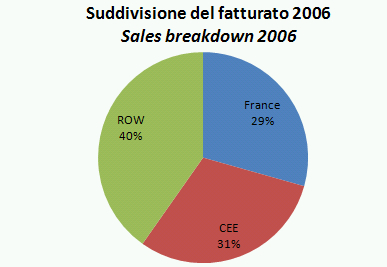

Cottin Freres opera come produttore di vini in Borgogna con una strategia sostanzialmente diretta al miglioramento del mix di prodotto. I vini DOC (che per loro sono Village, 1er Cru e Grand Cru) hanno raggiunto il 70% del fatturato e sono cresciuti nel 2006 del 12% circa. Il fatturato e’ come vedete molto ben bilanciato tra Francia (che cresce del 13% nel 2006), Europa e resto del mondo. Fuori dalla Francia il Regno Unito e’ il principale mercato del gruppo (+15% nel 2006). Il fatturato totale e’ cresciuto del 9% circa nel 2006 a causa del calo piuttosto significativo nel mercato europeo (ex Francia, -17%) e delle vendite praticamente invariate in Giappone (+2%) e USA (stabili). Cottin Freres operates as Burgundy wines producer with a strategy of improving its mix. Quality wines (Village, 1er Cru and Grand Cru) are 70% of sales and grew by 12% in 2006. Sales are well balanced between France (+13% in 2006), Europe and rest of the world. Outside France, UK is the key market (+15%). Sales were up 9% in 2006 due to the sharp decline in the European market (ex France, -17%) and of the flattish sales in Japan (+2%) and USA (flat).

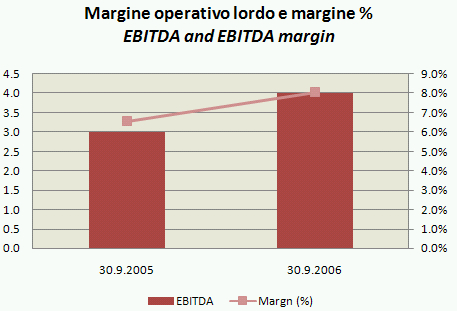

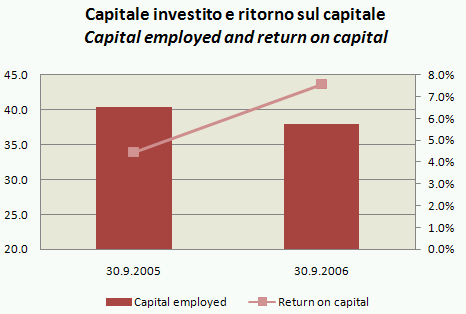

Cottin ha invece fatto molto bene nel 2006 dal punto di vista dei margini. La societa’ non ha dei margini particolarmente elevati. Non abbiamo dettagli, ma con un capitale investito di EUR38m e un fatturato di EUR50m e’ abbastanza presumibile che l’azienda non sia completamente integrata a monte nelle vigne ma comperi molto del suo prodotto. Il margine lordo (in questo caso dopo gli acquisti di uva e vino) e’ intorno al 28%. Dicevamo del miglioramento dei margini: nel corso del 2006 l’azienda ha aumentato il margine operativo lordo da EUR3m a EUR4m, portando il margine all’8% dal 6.6%. Ha fatto piu’ utili netti (da EUR1m a EUR1.6m), ha ridotto il debito da EUR15.7m a EUR12.3m anche e soprattutto grazie al contenimento del magazzino (da 242 giorni a 208 giorni) e dei crediti verso clienti (da 77 giorni a 67 giorni). Questo a consentito una leggera riduzione del capitale investito a EUR38m che, accoppiata all’eccellente andamento operativo, ha consentito di migliorare il ritorno sul capitale dal 5% a quasi l’8%. Cottin did very well in 2006 on margins. Margins are not very high but they improved significantly. We argue that with EUR50m sales and EUR38m capital employed the company is not very much integrated in vineyards and that it could buy a lot of wine. The gross margin (ie after the cost of grapes/wines purchases) is in the region of 28% and improved by around 2%. As a result, EBITDA was increasing from 3 to 4m EUR, with a margin moving from 6.6% to 8%. Net profiti improved by over 60% to EUR1.6m and debt moved down from EUR15.7m to EUR12.3m mainly thanks to the reduction of inventories (from 242 days of sales to 208) and receivables (from 77 to 67 days). This allowed a slight reduction of capital employed (from EUR40m to EUR38m, which coupled with the better operating results led to a higher return on capital (8% vs. 5%).

Che intenzioni ha Cottin Freres? Di continuare a investire nel miglioramento del mix ma soprattutto di comperare altre aziende vinicole per incrementare la sua dimensione. Non ha uno spazio elevato in bilancio (cioe’ il debito e’ ancora piuttosto elevato, a 3 volte il margine operativo lordo), ma con il titolo quotato in borsa potrebbe avere un altro strumento: potrebbe dare le proprie azioni al posto del denaro. La quotazione in borsa per un azienda del genere dovrebbe servire anche e soprattutto a questo. What are the plans of Cottin? To continue to invest in improving the revenue mix but most of all to buy other wine companies to increase its size. There is not a big room for that in the balance sheet, as the debt is still at 3 times EBIDTA (but quickly improving): however, having the stock listed there is another way to pay for an acquisition: you can issue new shares. For a listed company, this is also a key advantage of being listed.

Infine, vi metto una tabella di confronto con un po’ di aziende italiane che abbiamo di recente analizzato. Come potete vedere Cottin Freres non ha numeri stratosferici rispetto alle nostre grandi (!!) aziende vinicole. Ha margini inferiori a quasi tutte le aziende non cooperative, un ritorno sul capitale abbastanza allineato e una dimensione dignitosa ma sicuramente non gigantesca. Allora, sarebbe bello vedere qualche azienda italiana mettersi in gioco e andare in borsa (oltre a Giordano che un giorno o l’altro arriva). Finally, I put a table to compare a few Italian companies with Cottin Freres. As you can see, the French company does not stand out the sample of Italian companies whatever ratio (size, margins or return) you want to consider. This implies that it would be nice to see an Italian wine company going for the stock market (in addition to Giordano).

LVHM ha pubblicato a Febbraio i risultati 2007, di cui analizziamo specificatamente la parte relativa al vino e agli spirits. Anticipando la conclusione, i numeri indicano che LVMH sta performando come un orologio svizzero, con un ritorno sul capitale costante intorno al 12%, dei margini in leggero miglioramento (grazie alla parte spirits) e un fatturato in buona crescita (quasi +8%) essenzialmente guidato dai maggiori volumi. Cio’ ha spinto l’azienda a investire pesantemente nel 2007 nella divisione (EUR181m rispetto a poco piu’ di EUR100m nel 2006).

LVHM published its 2007 results, which we analyse only for the wine/spirits business. Figures show that the company is performing well, with a constant return on capital at 12%, slightly improving margins in the spirits business and a good top line growth (+8%), mainly driven by volumes. This allowed LVMH to invest heavily in 2007 (EUR181m vs. EUR100m in 2006).

Il fatturato cresce del 7.7% a EUR3226m, di cui EUR1802m nella divisione vino e Champagne (+7%) e EUR1424m nella divisione Cognac e spirits (+9%). E’ stato un anno essenzialmente guidato dai volumi, che sono cresciuti dell’8% a livello annuo, con una accelerazione nella seconda meta’ dell’anno (+9%), mentre il prezzo-mix e’ sceso leggermente (-0.5% nell’anno e -1% nel secondo semestre), essenzialmente a causa del peggioramento dei cambi (che hanno inciso negativamente per oltre il 5%). Come vedete, il peggioramento del prezzo mix ha essenzialmente inciso sulla parte vino/Champagne, dove il prezzo medio e’ sceso da 20.6 a 20.1 euro a bottiglia (!), mentre la parte Cognac/spirits e’ leggermente cresciuta, da 13.8 a 14.1 euro a bottiglia.

Sales were up 7.7% to EUR3226m in 2007, of which EUR1802m for wines and Champagne (+7%) and EUR1424m for Cognac/spirits (+9%). It has been a year essentially led by volumes, which were up 8% on a yearly basis, with an acceleration in H2 (+9%), while price mix slightly worsened (-0.5% for the year, -1% for H2), mainly due to the worsening of the exchange rates (over 5% negative impact). As you can see, the worsening of the price mix was just in the wine/Champagne division, from 20.6 to 20.1EUR per bottle, while for Cognac and spirits the company performed better, moving from 13.8 to 14.1 per bottle.

L’analisi del fatturato per area geografica ci ripropone il tema dei cambi, che ha chiaramente influenzato le vendite in USA, rimaste sostanzialmente stabili e raggiunte dall’Europa (Francia esclusa) che ha invece realizzato una crescita del 12% nel corso del 2007 (ma con un visibile rallentamento nella seconda parte dell’anno). In Francia il fatturato e’ cresciuto dell’8%, mentre in Asia a fronte di un ottimo primo semestre, nel secondo le vendite sono cresciute soltanto del 4%. Sempre molto bene la strategia di diversificazione geografica, con le vendite negli altri paesi in crescita del 20%.

Sales by region is highlighing the impact of exchange rates, which were clearly affecting US business, flat, while Europe was posting a very good 12% growth (but slowind down in H2). France was ok at +8%, while Asia had a slowdown in H2 at +4% after a double digit performance in H1. Still very good the diversification strategy, which led sales in other countries up 20%.

I volumi di Champagne sono cresciuti del 4% circa nell’anno, praticamente soltanto nel primo semestre (+9%), raggiungendo 62m di bottiglie nel 2007. Le vendite di Cognac sono andate meglio, con una crescita del 10% a 61m di bottiglie nel 2007, con una accelerazione nella seconda parte dell’anno (+12% contro il +8% del primo semestre). Per quanto riguarda le altre categorie, gli altri spirits hanno raggiunto 29m di bottiglie (con un recupero nel secondo semestre, +15% dopo un primo semestre stabile) mentre la divisione vino ha avuto ancora una volta un ottimo anno con una crescita del 13% dei volumi a 39m di bottiglie (+13.6% nel secondo semestre). Champagne volumes were up 4% in 2007, mainly achieved with the +9% of H1, at 62m bottles. Cognac sales were better at +10%, with a +12% in H2, reaching 61m bottles. Other spirits reached 29m bottles, with a good recovery in H2 at +15% after a flat H1, while wine business was again growing very well with volumes up 13% to 39m bottles (+13.6% in H2).

Passiamo ai margini, che sono stati in leggero miglioramento dal 32.1% al 32.8% in termini di margine operativo netto, segnando in valore assoluto una crescita del 10% a 1058m. Come vedete dal grafico, questa crescita e’ stata sostanzialmente merito della divisione Cognac che e’ passata dal 21.6% al 22.6%, mentre la parte vino e Champagne e’ rimasta stabile su un livello (stratosferico) tra il 45% e il 46%. Moving to margins, they improved slightly from 32.1% to 32.8% (EBIT) with a absolute value of 1058m (+10%). As you can see from the graph, this growth was essentially led by Cognac and spirits which moved from 21.6% to 22.6%, while wine and Champagne was flat at a huge level of 45-46%.

Passando al ritorno sul capitale ritorniamo sulla terra, con un livello stabile del 12%, a causa essenzialmente della crescita del capitale investito da EUR7.9bn a EUR8.7bn. Di questo capitale investito una parte molto significativa e’ rappresentata dai prodotti in fase di invecchiamento, che rappresentano un immobilizzo colossale, pari a circa EUR2.7bn, cioe’ un valore dell’83% circa del fatturato annuo. Return on capital is more normal, at around 12%, mainly due to the heavy growth of capital employed fro EUR7.9bn to EUR8.7bn. Of this capital, a significant portion is represented by ageing products, for roughly EUR2.7bn, which is a portion of roughly 83% of the yearly sales.

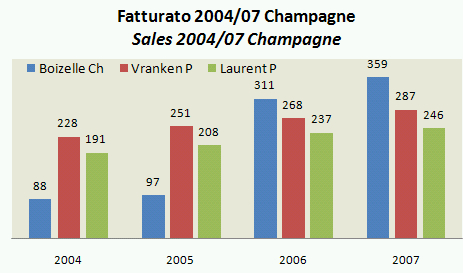

Parliamo oggi di Boizelle Chanoine, che ha appena fornito i risultati annuali e che e’ stato protagonista nel corso degli ultimi due anni di una crescita prodigiosa grazie all’acquisizione della Maison Burtin e di Champagne Lanson completata a Marzo 2006. Oltre a rappresentare il n.2 del mondo dello Champagne dietro a LVMH (che e’ tra tre e quattro volte piu’ grande), e’ interessante osservare l’azienda perche’ si possono apprezzare i forti miglioramenti che l’acquisizione ha portato sia in termini di margini delle aziende acquisite che in termini di ritorno per gli azionisti (rapidamente cresciuto grazie alla leva finanziaria). Come vedete da questo primo grafico, Boizelle ha molto velocemente preso piede superando sia Vranken Pommery che Laurent Perrier. Tra i suoi marchi ora figurano Burtin e Lanson, oltre a Boizelle, Chanoine e Philipponat.

We review today the operations of Boizelle Chanoine, which just released 2007 results and which strongly increased its business over the last 2 years on the back of the acquisition of Maison Burtin and Champagne Lanson completed in March 2006. Today, this company is the n.2 in the Champagne production after LVMH (which is much larger). It is very interesting because it shows how a company can strongly improve profits and return for its shareholders by carrying out acquisitions. As you can see from the first graph, Boizelle passed both Vranken and Laurent Perrier in terms of sales in 2006. Among its brands, you can now find Burtin, Lanson, Boizelle, Chanoine and Philipponat.

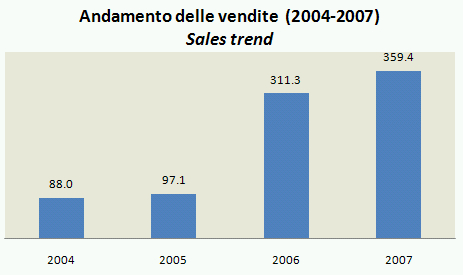

Il fatturato nel 2007 e’ cresciuto da 311m a 359m, +15%, sostanzialmente grazie al consolidamento delle nuove acquisite. Spaccando questo 15%, infatti, si nota come i volumi siano cresciuti del 3% a 21.6m di bottiglie, il prezzo mix e’ stato stabile, mentre un 12% di incremento e’ stato generato dall’inclusione delle nuove acquisite che nel precedente anno erano state consolidate soltanto a partire dal secondo trimestre. Sales in 2007 grew from 311m to 359m, +15% mainly thanks to the consolidation of the new companies. The breakdown of growth is: +3% volumes to 21.6m bottles, a stable price mix and a 12% increase deriving from the consolidation of the acquisitions from January in 2007 (vs. April in 2006).

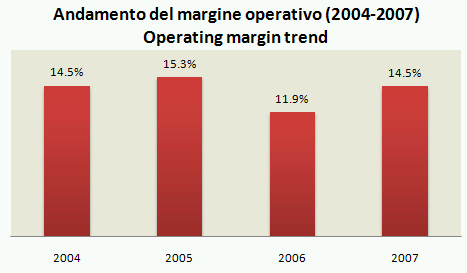

Vediamo cosa e’ successo ai margini del gruppo. Le acquisizioni hanno buttato giu’ i margini dal 15% al 12% tra il 2005 e il 2006, essenzialmente perche’ le societa’ acquisite avevano dei margini piu’ bassi (sia per il tipo di prodotto che per la piu’ limitata integrazione a monte nella produzione di uva). In realta’ e’ piu’ importante dire che l’utile operativo e’ passato da 15m a 37m e che l’utile netto e’ balzato da 8m a 15m tra il 2005 e il 2006. Nel 2007 invece si sono estratte le sinergie e il margine del gruppo e’ ritornato vicino al 15%, garantendo un altro anno di crescita esplosiva dell’utile operativo, +40% a 52m. E gli utili gli sono andati dietro, un altro +45% a 21m di euro (EUR25m se aggiustato per gli oneri straordinari). Quindi il risultato delle acquisizioni e’ stato veramente molto positivo: la Boizelle Chanoine e’ passata da essere una societa’ minore con meno di 100m di fatturato e 8m di utile a una azienda che fattura 360m e produce utili di oltre 20m di euro. Questo la mette in una prospettiva radicalmente diversa nel settore. La maggiore cassa che genera le consentira’ di crescere ulteriormente comperando altri operatori.

The trend of margin is the most interesting to see. The acquisitions were impacting negatively the operating margin which went down from 15% to 12% from 2005 to 2006 (acquired companies were less integrated in the production). It is however more important to note that operating profit moved up from 15m to 37m and that net profit nearly doubled from 8m to 15m between 2005 and 2006. In 2007, synergies started to flow through and Boizelle was back to its historical 15% margin, with another strong growth in absolute term (+40% to EUR52m). Net profit was following the same trend, +45% to EUR21m (EUR25m when restated for restructuring charges). As a result, acquisition were a big positive for Boizelle, which moved from a 100m sales/8m net profit to a 360m/21m range. This puts the company into a new perspective with more cash generation and more opportunity to further be an active consolidator in the Champagne segment.

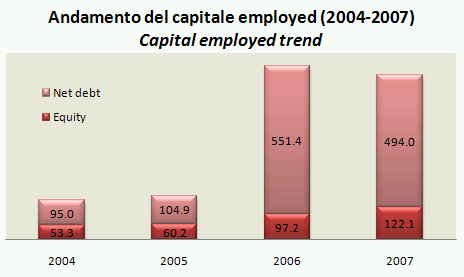

Le acquisizioni hanno ovviamente determinato un balzo del capitale investito, che vedete essere passato da 165m a 648m nel 2006, per poi ridiscendere a 615m nel 2007 grazie a una svendita dei magazzini che a valle delle operazioni era arrivato a 461m di euro (433m a fine 2007). Chiaramente queste operazioni hanno comportato dei significativi impatti sul debito, che e’ passato da 104m nel 2005 a 494m nel 2007. Il debito e’ estremamente elevato, ma e’ garantito dal magazzino che ha un valore di mercato quasi equivalente. Questo e’ un vantaggio delle aziende vinicole, e di Champagne in particolare (dato che hanno maturato questa consapevolezza del valore del loro magazzino). Acquisitions were also implying a jump of capital employed, moving from 165m to 648m in 2006 and to 615m in 2007. This small reduction occurred following are reduction of stocks from 461m to 433m. These operations were clearly implying a big jump of debt from 104m in 2005 to 494m in 2007. Debt is very high, but it is guaranteed by a stock of products which is very significant. This is an advantage of wine companies, which have big stocks but also an additional way to guarantee their borrowings.

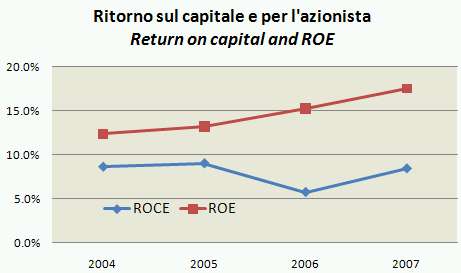

I ritorni sul capitale come vedete sono nell’ordine dell’8-9% sul capitale investito (con l’eccezione dell’anno dell’acquisizione), mentre il ritorno per l’azionista cresce dal 12-13% (post tasse) al 17.5% del 2007. Questo e’ il risultato della leva finanziaria: usare cioe’ i soldi degli altri (se te li danno!) e investirli con un ritorno superiore al tasso di interesse pagato, tenendosi quindi la differenza… The return on capital is in the region of 8-9% (with the exception of the year in which the acquisitions were made), while the return on equity moved from 12-13% to 17.5% in 2007. This is the result of the financial leverage: in other words, if you succeed in getting a higher return on the investment compared to the interest rate you pay, all the gap is additional money you put in your pocket.

Le esportazioni di Champagne sono andate a gonfie vele anche nel 2007, con un incremento del 10% a valore (a EUR2.37 miliardi di euro). Cio’ corrisponde a un volume di 110m di litri (circa 147m di bottiglie rispetto a un totale di oltre 320m). Come potete vedere, tutti gli indicatori sono positivi: i volumi crescono del 5.5% (rispetto a un +11% registrato nel 2006), il prezzo-mix migliora del 4.5% (+3.5% nel 2006 rispetto al 2005). Nel resto del post ci occuperemo di analizzare dove va questo Champagne e a che prezzo, e scopriremo che il mercato italiano e’ particolarmente appetibile in quanto accoppia una dimensione significativa a un prezzo medio molto piu’ elevato della media. Champagne exports for 2007 performed very well with a 10% increase in value (EUR2.37bn), implying 110m liters (147m bottles). As you can see from the graph, all indicators are positive: volumes are up by 5.5% (vs. +11% in 2006), price-mix improved by 4.5% (+3.5% in 2006 vs. 2005). In the rest of the post we will focus on geographical performance and we will discover that the Italian market is paritcularly appealing as it couplet a significant size with a very high average selling price.

Passiamo all’analisi geografica dell’export. Let’s move to the analysis by country:

• L’Inghilterra resta il primo mercato per lo Champagne: copre circa il 25% delle esportazioni a valore (EUR580m) e il 28% del volume (circa 42m di bottiglie), con un prezzo medio che viaggia sui 18 euro al litro rispetto ai 21.4 medi del 2007. E’ chiaramente il mercato a maggior crescita per lo Champagne, in quanto accoppia una dimensione significativa a un tasso di crescita sopra il 10% sia nel 2006 che nel 2007, in cui e’ cresciuto di quasi il 12%. Questa crescita appare anche molto ben bilanciata tra i volumi, che crescono del 4-5% annuo e il prezzo-mix, che fa la parte restante nonostante il graduale deprezzamento della sterlina contro l’Euro. • UK is the major market for Champagne, with 25% of exports by value (EUR580m) and 28% of volume (roughly 42m bottles). The average price is however below the average of exports (18EUR vs. 21EUR). This is clearly the key growth market for Champagne, as it couples a very large size with a double-digit growth in both 2006 and 2007. This growth is also well balanced between volumes (+4/5% both in 2006 and 2007) and price-mix, which is the remaining portion, despite the gradual devaluation of the currency vs. Euro.

• Il secondo e terzo mercato sono gli USA e il Belgio. Li metto insieme perche’ osservando i dati si nota che questi mercati si sono mossi in modo esattamente speculare, come se una parte delle esportazioni negli USA (passate da 409 a 236m di euro) fossero state automaticamente compensate dal Belgio (piu’ che raddoppiato da 125m a 325m di euro). Se prendiamo questi due mercati insieme, osserviamo una crescita del 5% nel 2007, rispetto a un +8.7% del 2006 e soprattutto inferiore al +10% del totale export. • The second and third markets are USA and Belgium. I put them together as looking at the figures these markets moved as a mirror, as if some export to the US of 2007 (moved from 409m to 236m) were passing from Belgium (which more than doubled from 125m to 325m euro). If you take these two markets together, you would get a picture of 5% growth in 2007 after a 9% in 2006, below the overall trend of exports.

• Dove sono dunque gli altri mercati dove lo Champagne e’ andato forte? Beh, partiamo con l’Italia che a dispetto dell’economia debole non e’ stata indietro neanche nel 2007, con un incremento del 10.3% a 216m di euro, esattamente in linea con il trend del totale export. Soprattutto, come vedete dal grafico l’Italia e’ il miglior mercato in termini di prezzo di vendita tra i grandi mercati di esportazione dello Champagne (28 euro contro 21 di media). Per trovare un mercato dove i prezzi sono migliori, bisogna scendere al Canada (30) che pero’ importa 1.1m di litri contro i 7.7m dell’Italia. Quello che in Italia nel 2007 non ha funzionato sono stati i volumi, che sono invece scesi del 2% nel 2007, dopo pero’ un grande balzo (+18%) dell’anno precedente. • What are the other good markets? Starting from Italy, we note that in 2007 exports were good at +10.3% or EUR216m, in line with the total figure. As you can see from the graph Italy is also the country among large ones which is buying Champagne at the highest price (better mix, 28EUR vs. 21EUR average). To find a market where prices are better, you would need to go to Canada (30EUR) with 1.1m liters vs. 7.7m of Italy. What in Italy did not work in 2007 were volumes, which were down 2% after the big jump recorded in 2006 (+18%).

• Torniamo ai mercati in crescita: Singapore (+24% a 157m di euro), Spagna (+30% a 80m di euro) e Svezia (+37% a 31m di euro). I mercati meno performanti invece sono stati la Svizzera a +3% e il Giappone a -7%. • Back to growth markets: Singapour was +24% to 157m, Spain +30% to EUR80m and Svezia (+37% to 31m). Underperforming markets are Switzerland with +3% and Japan with -7%.

[TABLE=44]

Questo blog non rappresenta una testata giornalistica in quanto viene aggiornato senza alcuna periodicità. Non può pertanto considerarsi un prodotto editoriale. Le immagini inserite in questo blog sono tratte in massima parte da Internet; qualora la loro pubblicazione violasse eventuali diritti d'autore, vogliate comunicarlo a mbaccaglio@gmail.com, saranno subito rimosse.