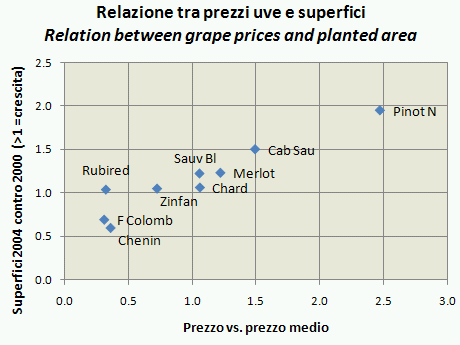

Fonte: www.wineinstitute.org

Gli Stati Uniti hanno avuto nel 2007 un anno molto positivo per le esportazioni di vino, ovviamente guidate dalla California, che rappresenta circa il 95% del totale. Il valore ha raggiunto il massimo storico di USD951m, pari a EUR614m usando il cambio attuale. Sempre poco rispetto a quanto si fa in Italia (circa EUR3.5bn) o in Francia (oltre EUR6bn), pero’ come potete notare dal grafico degli ultimi anni la progressione e’ molto chiara. Stiamo parlando di un incremento dell’8.5%, molto simile a quello italiano (circa 9%) e superiore a quello francese (+6%). In un’ottica quinquennale l’andamento e’ stato ancora piu’ positivo, con una crescita media annua del 12% circa. Va detto, a spiegazione del tutto, che la debolezza del dollaro contro praticamente tutte le valute del mondo ha favorito (e sta favorendo) le esportazioni americane nel mondo.

USA posted a very good year for wine exports, driven by California products, which represent roughly 95% of the total. In value, exports reached USD951m, or EUR614m. It is still lower than what Italy or France export (EUR3.5bn and EUR6bn), but as you can see from the first graph the progression over the past year has been significant. The increase was 8.5%, very similar to the 9% increase posted in Italy and better than the +6% of France. Looking more long term, in the last 5 years export CAGR touched 12%. All this is clearly helped by the weak USD which is favouring US goods exports.

Andiamo nel dettaglio: le esportazioni sono ammontate a 4.5m/hl, con un incremento del 12% rispetto al 2006. Tale incremento e’ in realtà superiore alla media annua degli ultimi 5 anni, che mostra una crescita del 10% circa dal punto di vista dei volumi. A questo si e’ quindi associato un leggero peggioramento del mix di vendita, che e’ passato da 2.16USD al litro a USD2.10 (EUR1.35). Ancora una volta, visto in un’ottica piu’ di lungo termine (secondo grafico) si puo’ apprezzare come il prezzo-mix delle esportazioni americane mostri un andamento leggermente positivo nel corso degli anni. Di nuovo a titolo di confronto, noi italiani esportiamo a EUR1.84 al litro, mentre i nostri amici francesi (anche grazie allo Champagne) viaggiano su uno stellare 4.3EUR al litro).

Volumes were 4.5m/hl, with a 12% increase vs. 2006. This is better than what posted in the last 5 years (10% compound). This implies a slight worsening of the mix in 2007, which moved from USD2.16 per liter to USD2.10 (EUR1.35). Once again, looking at a longer term graph you can easily see that the mix of US exports is gradually improving over the years. As a comparison, consider that Italian wine exports are carried out at an average of EUR1.84 per liter and French exports (also thanks to Champagne) at EUR4.3 per liter.

Vediamo dove esportano gli USA e come sono andati i diversi mercati. Beh, per tagliare corto potremmo dire che i mercati che hanno performato meglio sono quelli emergenti, mentre nei grandi mercati di consumo del vino le cose non sono andate cosi’ bene. E’ vero, in Europa (principale mercato con circa 2.6m/hl) i vini USA hanno perso il 3%, tutto per colpa di un 10% di peggioramento del prezzo mix, fatto molto strano in un anno in cui il dollaro ha giocato a favore. Vero invece e’ che in un mercato tanto interessante quanto il Canada (e noi italiani lo sappiamo molto bene), gli americani fanno un +23% con un +15% di volumi (0.8m/hl) e un +8% di mix (contro il nostro timido +3%). Gli americani esportano a USD2.9 al litro contro i nostri EUR3.6 (solo per i vini imbottigliati). Il prezzo mix in peggioramento del 16% e’ anche il principale commento da fare sul terzo mercato di esportazione, il Giappone, che copre circa 0.3m/hl di volume. Negli altri mercati le cose vanno a gonfie vele: il grafico vi mostra un bel balzo in Svizzera, che per importanza e’ ora il quinto mercato (considerando l’UE un mercato solo, naturalmente), in Corea e Cina, che ora sono il sesto e settimo mercato. In Cina gli USA esportano vino per USD16m, noi per EUR16m. Soltanto grazie al cambio EUR/USD a questo livello innaturale possiamo nascondere l’insuccesso del vino italiano in Cina…

Geographical break down. We might conclude that emerging markets performer well and developed markets not, but it would be not too precise. It is true that Europe was down 3% and this is the most important market for US wine exports with 2.6m/hl, due to a 10% worsening of the mix, which is quite difficult to understand given the benefit of the weak dollar. On the other hand, Canada performed very well with a 23% increase, of which 15% more volumes to 0.8m/hl and 8% better mix (vs +3% for Italian wine exports in Canada). US wine in Canada is sold at USD2.9 per liter vs. our EUR3.6. The price mix is also sharply worsening in Japan, with a -16%, which is the n.3 market for exports with 0.3m/hl. In the other markets the performance is by far better: Switzerland is up strongly and now is the market n.5. Korea and China are now n.6 and n.7. In China US are exporting wine for USD16m vs. our exports of EUR16m. Only thanks to the favourable USD rate we can say that we export more than US in this market…