Come abbiamo avuto modo di commentare recentemente, Vranken Pommery e’ probabilmente la maison che e’ andata meglio nel 2008. Il fatturato e’ rimasto stabile e i margini operativi hanno tenuto, e questo e’ gia’ un gran bel risultato (che diventera’ evidente quando analizzeremo i risultati degli altri). Il profilo degli utili (-7%) e’ stato pero’ colpito dai tassi di interesse (mediamente piu’ alti del 2007) ma soprattutto dalla politica di continuare a far crescere il magazzino (e quindi alzando i debiti) affinando piu’ a lungo i prodotti. Stiamo parlando di ormai 2 anni di fatturato del gruppo. Se non avessero magazzino, non avrebbero debiti. Per ora, il magazzino funziona come garanzia bancaria. Cosa succedera’ domani non lo so, di certo lo Champagne resta un marchio cosi’ forte che probabilmente la rivalutazione del magazzino e’ comunque un buon investimento. Cosa succedera’ nel 2009? Vranken Pommery parla di una vendemmia presumibilmente meno ricca della precedente (e’ la prima volta che esce questo tema) e dell’esigenza di proteggere i marchi e i prodotti di alta gamma, obiettivo che sara’ raggiunto proprio grazie al magazzino. Cosa stimano gli analisti? Un fatturato in calo del 2-3%, un MOL sostanzialmente stabile e un utile netto che scende del 20% (dopo il -7% del 2008).

As we have comment recently, Vranken Pommery is probably the Champagne house which performed better in 2008. The turnover was stable and operating margins were slightly up. The profile of net profit (-7%) was affected by interest rates (on average higher than in 2007) but also due to the policy to continue to raise inventories, which led to higher debt. We are now talking about 2 years of sales of the group. Without stock, they would not have any debts. For now, the value of inventories is used as a bank guarantee. What will happen tomorrow I do not know, of course Champagne is a strong brand and probably the strong revaluation of the stock is a good investment anyway. What will happen in 2009? Vranken Pommery is the first to anticipate a less rich harvest and the need to protect the high-end brands, an objective that will be achieved thanks to the huge inventories. What are the analysts estimates? A decline in sales of 2-3%, a broadly stable EBITDA and net income falling by 20% (after 7% in 2008).

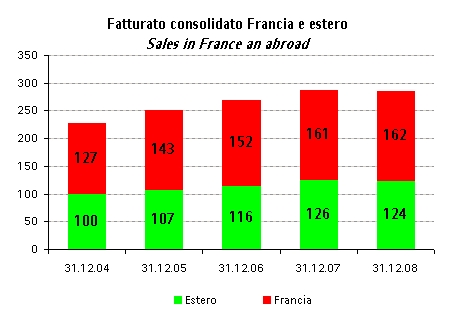

Dunque, le vendite sono scese dello 0.3% a 286 milioni, ma in realta’ le vendite di Champagne sono salite dell’1% a 268 milioni. In Francia il gruppo e’ andato bene, con un +0.7% sullo Champagne. Vista nell’ottica degli ultimi anni, si tratta di una battura di arresto, va pero’ detto che anche nel durissimo quarto trimestre dell’anno (quello dove si fa la meta’ del fatturato), le vendite hanno tenuto.

Sales fell by 0.3% to 286 million, but Champagne sales rose 1% to 268 million. In France the group was ok, with a +0.7% on the Champagne. Looking at the past few years, it is clear that there is a consolidation, but it must be underlined that even in the very tough fourth quarter (the one where 50% of sales are booked), sales were flat.

I margini operativi sono stati positivi: il MOL e’ passato da 60 a 62 milioni (+2.6%), con un margine in progresso dal 21% al 21.6%, raggiunto grazie al miglioramento del margine industriale di 1 punto percentuale. Gli oneri finanziari sono invece passati da 22 a 26 milioni e cio’ ha determinato la riduzione dell’utile netto da 18 milioni a 17 milioni (-7%, -8% se si aggiusta per i componenti non ricorrenti).

The operating margins have been positive: EBITDA increased from 60 to 62 million (+2.6%), with a margin in progress from 21% to 21.6%, achieved through the enhancement of industrial margin of 1 percentage point. Borrowing costs have risen from 22 to 26 million and this led to a reduction in net profit from 18 million to 17 million (-7%, -8% if you adjust for non-recurring).

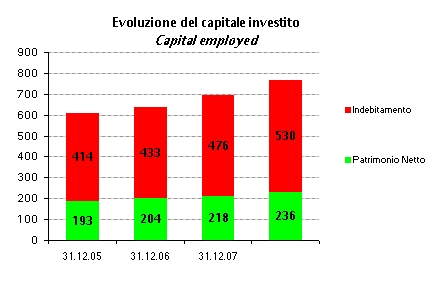

Veniamo al punto piu’ interessante di questo bilancio. Il capitale circolante continua a crescere (188% del fatturato a fine 2008), essenzialmente a causa del magazzino (552 milioni di euro), mentre sia i crediti verso clienti e i debiti verso fornitori sono scesi. Cio’ corrisponde a un aumento di 40 milioni, che insieme ai 12 milioni di investimenti ha piu’ che compensato la generazione di cassa pre-tasse di 29 milioni. Cosi’ il debito passa 476 milioni a 530 milioni (contando anche tasse per 8 milioni e 7 di dividendi), portando il capitale investito a 766 milioni (+10%).

The working capital continued to rise (188% of turnover at the end of 2008), primarily because of the stock (552 million), while receivables and payables decreased. This implied a working capital increase of 40 million, that with 12 million investments more than offset the pre-tax cash flow of 29 million. Debt moved from 476 million to 530 million (also factoring in tax for 8 million and dividends for 7), raising the capital invested to 766 million (+10%).

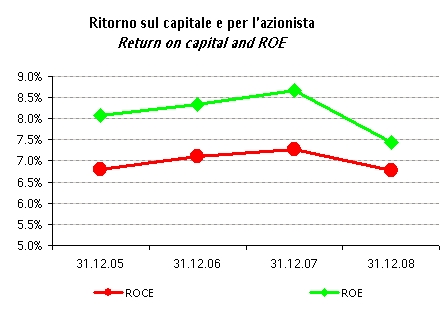

Questo forte incremento del capitale investito sta impattando il ritorno sul capitale, sceso dal 7.3% al 6.8%. In realta’, se Vranken riuscira’ a tenere gli utili (non e’ detto) grazie al magazzino che ha costruito, questo ritorno potrebbe anche essere interessante. E’ ora il turno degli altri. Credo che ne vedremo delle belle.

The sharp increase in investment is impacting the return on capital (from 7.3% to 6.8%). In reality ‘, if Vranken is able to keep the profits thanks to the inventories build up, this return could also be interesting. Is now the turn of other Champagne houses. I believe with much less appealing figures.