Dopo aver capito cosa fa LVMH proviamo a guardare a quanti soldi fa e a quanto cresce.

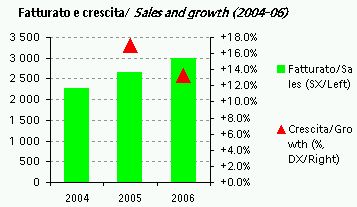

Il fatturato e’ salito di circa il 17% nel 2005 (grazie a una acquisizione nel campo degli spirits) e del 13% nel 2006. Come si suddivide questa crescita? Come per tutti gli operatori premium nel mercato, anche LVMH punta decisamente sul prezzo e sul mix. Nel 2006, a fronte di un +13% del fatturato, i volumi hanno contribuito per il 6.6%, mentre la combinazione di prezzi, mix e cambi (quest’ultima probabilmente negativa) hanno portato il resto. Dal punto di vista delle aree geografiche,

After a brief introduction of LVMH activity, let’s give a look to how much money it makes and how much it grows.

Sales were +17% in 2005 (also boosted by acquisitions) and +13% in 2006. How this growth is generated? As for all the players in the high quality wine and spirits, price-mix is an important component. The 13% growth reported in 2006 was made for just 6.6% by volumes, while the combination of price, mix and currencies (this almost surely negative) were bringing the rest.

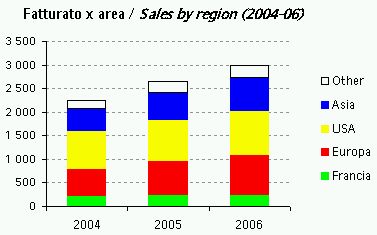

Dal punto di vista geografico, bisogna dire che il successo di LVMH nel mondo del vino negli ultimi 2 anni si chiama Europa e Asia escluso Giappone. Questi mercati sono cresciuti sensibilmente di piu’ degli altri: l’Europa viaggia intorno al 20% di crescita annua, l’Asia sul 23-25% nonostante il Giappone tiri di meno. La Francia non e’ praticamente cresciuta nel 2006, gli USA, complice anche il cambio, sono stati sul 5-6% di crescita.

Looking at differente geographical regions, we must say that the success of LVMH wines lies in two markets: Europe and Asia ex Japan. In Europe, sales are growing at a speed of around 20%, while in Asia growth is at 23-25% despite Japan which runs at much slower rates. France was basically flat in 2006, while US, also due to the negative forex, were up just 5-6%.

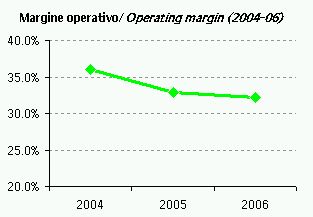

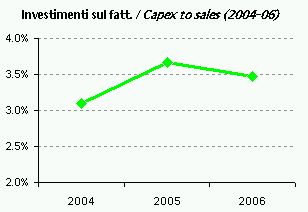

Passiamo ai margini, che sono credo i piu’ elevati che ci sia capitato di incontrare: il margine operativo e’ al 32% (ma era addirittura il 36% nel 2004), presumibilmente piuttosto simile per il segmento vini (Champagne e vino) e quello spirits (Cognac e altri). A guardare i numeri del primo semestre 2007, in cui le due aree sono suddivise, i margini sono molto simili. Gli investimenti, che trovate nel grafico successivo si posizionano sul 3-4% del fatturato.

Margins are instead at the top end of the industry, I think that I have not seen any firm with such high margins before: 32% of EBIT margin (but was even 36% in 2004), probably quite comparable between wines and spirits divisions. Looking at H1 figures, in which the two areas were split, the margins are very similar. Capex are around 3-4% of sales.

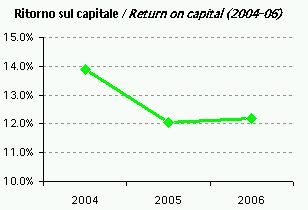

Il ritorno sul capitale? Siamo su livelli meno eccellenti che per gli altri numeri. I marchi hanno il loro peso. LVMH ha un ritorno sul capitale investito del 12% circa, in discesa dal 14% del 2004.

The return on capital is on less extraordinary level than other indicators for the company, as the brands have their weight in the capital employed: 12% in 2005 and 2006 vs. a level of 14% of 2004.