[English version inside]

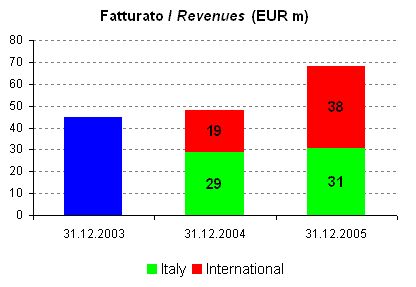

Frescobaldi e’ una delle grandi aziende che ancora mancavano all’appello della nostra analisi di bilancio. E’ anche la societa’ che nel 2005 ha scalato di piu’ le classifiche del mondo del vino italiano, e quindi ero un pochino curioso di leggere come mai. Bene, il suo fatturato e’ salito del 7.6% nel 2004 e del 42% nel 2005, toccando quota EUR68m. Il balzo del 2005 e’ da attribuire a: (1) l’acquisizione di Luce ; (2) un giro contabile per 4.7m riguardante le scorte americane che sono state riacquistate e rivendute, avendo quindi un impatto neutro sugli utili ma gonfiando il fatturato. Detto questo (e quindi ipotizzando che il fatturato sarebbe dovuto essere di circa 63m), il consolidamento di Luce ha fondamentalmente aiutato le vendite estere, che sono raddoppiate contro un +6% del fatturato italia, raggiungendo cosi’ il 55% del totale.

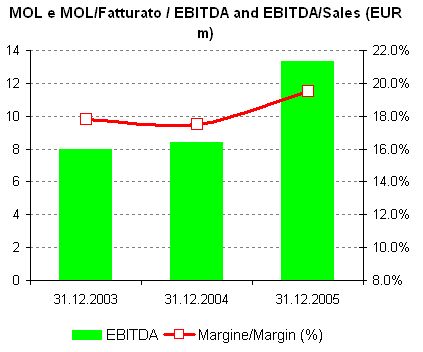

Margini. I margini sono medi, soprattutto considerando il livello a cui arrivano alcuni suoi concorrenti come Antinori, i quali stanno ben al di la’ del 30%. Il Margine lordo sulle vendite sta al 20% circa, in salita dal 17.5% del 2004, probabilmente grazie al consolidamento delle societa’ acquisite. Tutte le voci di costo sono un po’ piu’ alte di quelle di Antinori: le materie prime sul fatturato vanno al 38% (contro 25%), il costo del personale pesa per il 21% (in miglioramento rispetto al 24% ma sempre oltre il 16% di Antinori). A livello di margine netto, e riaggiungiendo l’ammortamento per la differenza di consolidamento (cioe’ quello derivante dal sovrapprezzo pagato per Luce rispetto al suo valore di libro), il margine operativo netto e’ salito dal 10% al 12%, raggiungendo 8.4m. I margini di Frescobaldi vanno pero’ letti nell’ottica della grande crescita raggiunta e del giochetto sul magazzino americano (che ha avuto un impatto negativo per circa il 2%).

Frescobaldi nel 2005 e’ cresciuta da 8m di MOL a 13m +58% e da 5m a 8.4m di utile operativo prima del goodwill +71%: in un anno di crescita cosi’ rilevante i margini non sono la prima cosa da commentare! Siccome l’acquisizione e’ stata pagata con debito, a livello di utile netto le cose sono andate meno bene, con un utile rettificato di circa 3m rispetto a 2.5m del 2004 e con un utile non aggiustato in crollo da 4.4m a 2.6m.

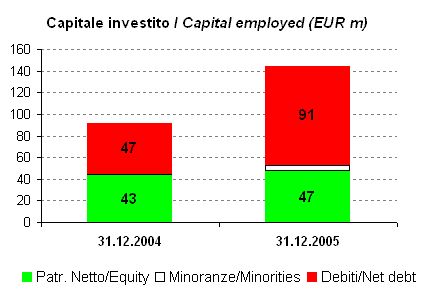

Struttura finanziaria. Beh, il debito e’ raddoppiato da 47m a 91m a fronte dell’acquisizione. Il livello e’ eccessivo a 6.8 volte il MOL, ed e’ per questo motivo che Frescobaldi ha venduto una quota di minoranza di una sua tenuta (per un ammontare non conosciuto) al fine di ridurlo… vedremo il debito a fine anno. Comunque il capitale investito e’ salito a 144m da 91m del 2004.

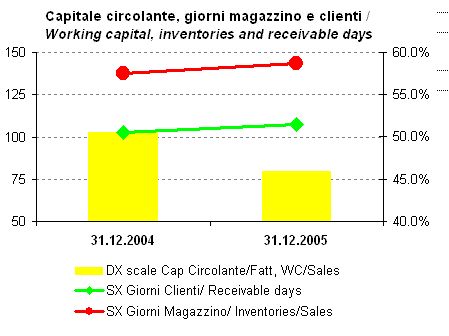

Il capitale circolante e’ tutto sommato meno significantivo di alcuni suoi concorrenti, al 45% del fatturato. Cio’ anche grazie al basso livello dei giorni cliente (poco sopra 100), a mio avviso grazie alla forte esposizione estera del gruppo (dove a differenza che in Italia, si paga con dei tempi molto piu’ brevi).

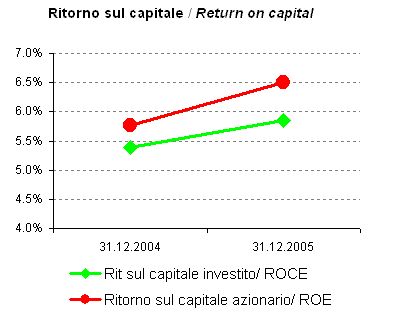

I ritorni sono piuttosto bassi, anche se in crescita rispetto allo scorso anno. Siamo sul livello del 6.5% per il ROE dopo le tasse e poco sotto il 6% per il ritorno sul capitale investito pre-tasse… vedremo cosa e’ successo nel 2006.

Frescobaldi is one of the major firms which we did not analyse yet. It is also the company which in 2005 moved up the most in the ranking of domestic wine producers. I was therefore a bit curious about the reasons of this jump. Revenues were +7.6% in 2006 and +42% in 2005, at EUR68m. The increase in 2005 was due to (1) the acquisition of Luce… (2) an accounting issue, for which the company booked EUR4.7m additional revenues and costs as it bought the US inventories from the previous distributor and resold them to the new one. Restating from this item, revenues would have been EUR63. The change in consolidation perimeter was very evident in the international business which doubled vs. a just +6% for Italy. Export now is 55% of total sales.

Margins are not high, also considering the high level reached by some of Frescobaldi competitors, such as Antinori (well above 30%). The EBITDA margin is at 20%, improving from 17.5% of 2004, probably thanks to the consolidation of new companies. All the cost items are a bit higher than Antinori: personnel costs are at 21% (better than 24% of 2004 but above 16% of Antinori), raw materials are 38% against 25%. In terms of EBIT margin (adding back the goodwill depreciation) we get to 8.4m EUR, or 12% of sales (increasing from 10% of 2004. All in all,

Frescobaldin posted a jump of EBITDA from EUR8m to EUR13m, +58% and from 5m to EUR8.4m for EBIT (+71%): in other words, this has been a terrific year for growth and in these years margins are probably not the first thing to look at. Since the acquisition was paid with debt, net profit was less exciting, moving from 2.5m to EUR3m.

Financial structure. Debt doubled from EUR47m to EUR91m due to the acquisition. The level is now probably too high at 6.8x ratio over EBITDA, and for this reason Frescobaldi decided to sell a minority stake of one of its properties (no detail on the price) in order to reduce it… we will see what has been the impact in 2006. The capital employed moved from EUR91m to EUR144m in 2005.

Working capital is less heavy than for some of its competitors at 45% of sales. This is both thanks to lower level of receivable days (less than 100 days), probably thanks to the high exposure to international sales (where unlike Italy payments are much quicker).

The return of capital is pretty low. It stands at 6.5% for ROE after tax and just above 6% for ROI… we have to see what happens in 2006 when the new consolidation perimeter will start to work together.