Fonte: Mediobanca research

Sono stati pubblicati i dati di Mediobanca relativamente alle principali societa’ italiane. Siamo quindi nella condizione di aggiornare le classifiche che abbiamo lanciato qualche mese fa relativamente al fatturato, al valore aggiunto, ai margini operativi e via dicendo. Partiamo con il fatturato, specificando che rispetto alla classifica originale di Mediobanca ho apportato le seguenti modifiche (1) ho aggiunto Campari per la sua parte vino, (2) ho inserito i dati consolidati di Santa Margherita (invece di quelli riferiti alla capogruppo).

Mediobanca published its data on the main Italian companies. We extracted the key operators of the wine business and we are therefore able to update all the rankings we launched for 2005 data a few months ago. The key changes we took are (1) the inclusion of Campari wine division and (2) the addition of Santa Margherita consolidated figures vs. the parent company ones.

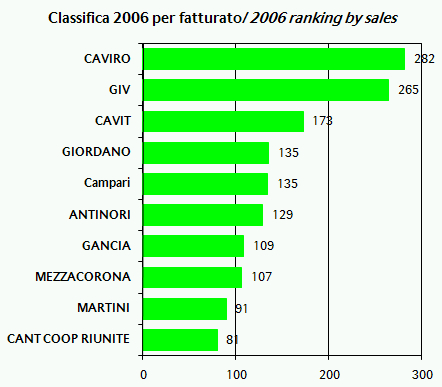

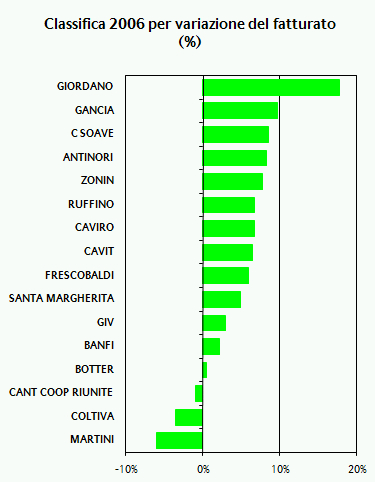

Nel 2006, secondo il campione Mediobanca (indagine sul vino) il fatturato era in crescita del 5%. Possiamo subito anticipare che delle 18 societa’ qui incluse 11-12 hanno superato questa asticella e, quindi, dovrebbero avere guadagnato quota di mercato. La seconda cosa importante da dire e’ che Giordano ha superato Antinori e Campari nella classifica ed e’ diventata, almeno in base al fatturato, il primo operatore italiano privato nel mondo del vino.

In 2006, according to Mediobanca survey, sales growth in the wine business averaged 5%. We can anticipate that among the 18 companies we are analyzing here, 11-12 did better than this. The second important thing to derive here is that Giordano exceeded Campari and Antinori and became in 2006 the private wine producer n.1 in Italy.

Il mercato e’ ancora guidato dalle tre cooperative, Caviro, GIV e Cavit. E’ pero’ piuttosto evidente che delle tre soltanto Caviro nell’ultimo biennio sia riuscita a mantenere una crescita comparabile a quella delle cantine private. In particolare, GIV, passata da 236m a 265m ha perso terreno rispetto a Caviro che era molto vicina nel 2004 (238m) ma che oggi svetta con 282m, facendo segnare una crescita media del fatturato del 9% circa rispetto al 6% della costellazione GIV. Piu’ sotto, Cavit ha una fatturato stabile, nel senso che nel 2006 ha recuperato quello che ha perso nel 2005. Tra le aziende private Giordano e Antinori (e Campari, anche se in questo caso parliamo di una divisione e non del “core business”) si giocano la leadership: a livello di fatturato, Giordano ha in questi due anni chiaramente surclassato Antinori, con una crescita annua di oltre il 15% annuo contro il 9% di Antinori. Con 135m e 129m di fatturato, le due aziende sono comunque molto vicine. La prossima quotazione in Borsa di Giordano potrebbe dare ulteriore spinta all’evoluzione di questa societa’, che gia’ potete vedere essere la prima societa’ del 2006 tra le grandi in termini di tassi di crescita.

The market is still led by three cooperatives: Caviro, GIV and Cavit. It is however quite evident that only Caviro is able to maintain a sales growth similar to the private operators. GIV moved in 2 years from 236m to 265m in sales and lost ground vs. CAVIRO, which in 2004 was at the same level (238m), while in 2006 it is the undisputed leader with 282m. Caviro grew by 9% yarly vs. 6% of GIV and 0% for CAVIT. Among the private operators, Giordano exceeded for the first time Campari and Antinori in terms of revenues and became with EUR135m the first private wine producer in Italy. It grew by 15% yearly in the last 2 years, vs. 9% of Antinori. The forthcoming IPO of Giordano could allow the company to become even more aggressive in terms of growth.

Sotto i primi 6 ci sono Gancia e Mezzacorona, che sono entrambe sui 107-110m anche se Mezzacorona sembra avere un passo migliore. Cantine Riunite hanno continuato a perdere fatturato (-1% a 81m), cosi’ come Martini (-6% a 91m). Al 13 posto si conferma Frescobaldi, che dopo il balzo del 2005 ha fatto segnare un +6%, mentre al n.14 Zonin ha recuperato quello che ha perso nel 2005. In questa fascia dimensionale si inserisce il consolidato di Santa Margherita, n.12 nella classifica.

Below the first 6 places there are Gancia and Mezzacorona, which are at around 107-110m of sales. Of these, Mezzacorona seems to growth at a better rate. Cantine Riunite lost 1% in 2006, similarly to Martini (-6%). At n.13 there is Frescobaldi which grew by 6% after the jump of 2005, while n.14 is still Zonin, which recovered the sales lost in 2005. In this size class, we should mention Santa Margherita which with 73m of consolidated sales is the n.12 in Italy.

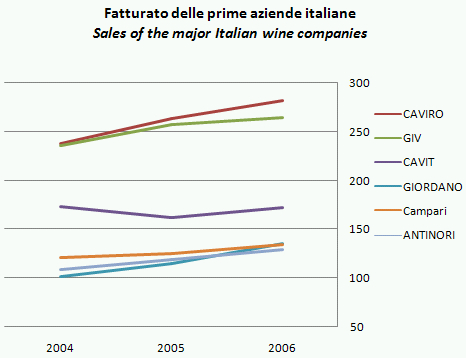

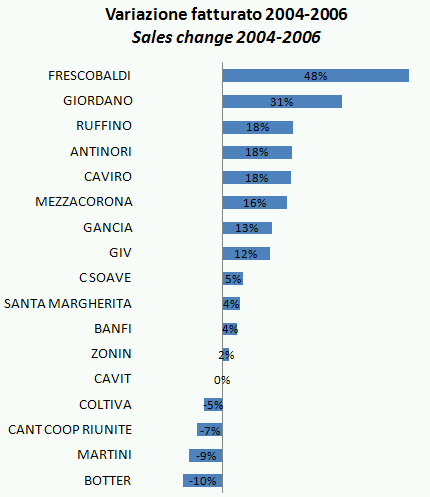

In questi due grafici vedete piu’ distintamente il percorso di crescita delle aziende principali. Frescobaldi, e Giordano sono quelle che nel biennio 2004-2006 sono cresciute di piu’. Su ritmi vicini al 10% annuo si pongono Antinori, Caviro e Ruffino. Tra i nomi famosi in fondo alla classifica Cantine Riunite, Zonin e Cavit.

In the two final graphs you can find the growth in 2006 and in 2005-06 of these companies. Frescobaldi and Giordano are at the top of the 2-years ranking, while with a pace of close to 10% p.a. we find Antinori, Caviro and Ruffino (Constellation Brands). Among the famous ones, Cantine Riunite, Zonin and Cavit are at the bottom of the ranking.